From the earliest days of human interaction, trade has been the cornerstone of societal progress. Picture the bartering of goods in ancient marketplaces: a farmer trading grain for a craftsman’s pottery. As societies evolved, so too did the mechanisms for exchanging value. Coins minted from precious metals replaced bartering; eventually, government-run paper money took center stage. Today, we stand at the precipice of another transformation: the shift from fiat currency to digital assets. This evolution reflects humanity’s quest for efficiency, security, and inclusivity in financial systems.

Stablecoins represent a pivotal chapter in this ongoing story of money. These digital currencies, designed to maintain a stable value, have become the backbone of decentralized finance (DeFi). In 2019, the total market capitalization of stablecoins was a modest $1 billion. By 2024, this figure had exploded to over $130 billion (source: CoinGecko). Even more striking, in the second quarter of 2024, stablecoins processed approximately $8.5 trillion in transactions, surpassing Visa’s $3.9 trillion in the same period (source: Benzinga). This remarkable growth underscores their role as essential instruments for trading, lending, and cross-border transactions in the digital age.

Nobel Prize-winning economist Milton Friedman once said, "The Internet is going to be one of the major forces for reducing the role of government. The one thing that’s missing, but will soon be developed, is a reliable e-cash." Stablecoins answer that call, combining the internet's borderless nature with the stability of traditional currencies. Leaders like Circle (USDC) and Tether (USDT) represent fiat-backed stablecoins, heavily reliant on centralized fiat reserves. In contrast, MakerDAO’s DAI is an innovation as a decentralized stablecoin backed by ETH, the native digital asset of the Ethereum blockchain.

The stablecoin landscape has also witnessed disruptive experiments. Terra’s UST, which operated on an algorithmic model, ultimately collapsed, leaving a negative mark on the industry. On the other hand, emerging models like Ethena leverage delta-neutral hedging strategies to maintain their peg, and Usual tie their value to U.S. Treasury bonds. These innovations introduce a groundbreaking reality: digital money—unlike fiat—is programmable. Through blockchain, stablecoins acquire properties that enhance their utility. They not only function as fiat-equivalent mediums of exchange but also unlock new income streams and value propositions through their programmability.

This programmability revolutionizes money’s role in the economy. Stablecoins can power complex financial strategies, generate yield, and integrate into decentralized applications to create added utility. This evolution reshapes the financial landscape, offering possibilities far beyond traditional fiat currencies.

USH is at the forefront of this innovation. Building on the lessons of past stablecoin models, USH introduces robust mechanisms to maintain its peg and ensure stability. Its incentive structures are meticulously designed to enhance liquidity by generously rewarding liquidity providers. By integrating deeply into the MultiversX ecosystem, USH not only strengthens the ecosystem’s stability but also redefines how stablecoins can drive growth and utility in decentralized finance.

In this research paper, we unravel the story of money’s next great chapter, where decentralization, transparency, and accessibility redefine the boundaries of what’s possible in the world of finance.

Liquidity is among the most critical metrics of any crypto DeFi ecosystem, directly influencing the efficiency and overall health of the system. It allows users to access better pricing, lower transaction costs, and ensures smoother and more efficient market DeFi operations. In this framework, stablecoins play an instrumental role, acting as one of the most important tools for bootstrapping liquidity.

Many DeFi primitives greatly benefit from increased stablecoin liquidity:

For example the big demand for stablecoins on Hatom led to stables pools utilization rates drastically increasing, which resulted in an extremely high supply APY for stablecoins. It drove up yields, however this also resulted in significantly higher borrowing APYs for users, which made borrowing stables unaffordable for many users.

Stablecoins, as a liquidity mechanism, help maintain market stability, enabling traders and investors to hedge against volatility. A high level of stablecoin liquidity is generally considered a sign of a robust and healthy DeFi environment. However, MultiversX has struggled with attracting and retaining stablecoin liquidity.

During the last bull market, MultiversX saw a peak of over $50 million in liquidity, which was a significant achievement for the protocol. Yet, over the past years, liquidity has steadily declined, largely due to the broader market retracement driven by the bear market conditions. The liquidity reduction has left the platform with a noticeable gap in its DeFi competitiveness that needs to be addressed.

There are several reasons why liquidity, particularly stablecoin liquidity, has not rebounded as quickly as desired:

1. Friction in Onboarding New Liquidity

MultiversX has faced, and continues to face, significant challenges in attracting new liquidity from multiple sources. Users often encounter complex UX, high bridging costs, and the lengthy process required to bridge assets across chains. These barriers make it difficult for liquidity providers to justify bringing capital into the ecosystem. Users are dissuaded by the time, effort and costs required to move assets into MultiversX from other blockchains.

2. Lack of Chain Awareness

As a relatively new blockchain, MultiversX is struggling with low brand awareness in the broader crypto space. This lack of awareness undermines its credibility, a key factor in gaining the trust of liquidity providers. Without a clear and established track record, potential new users are hesitant to bring liquidity to the protocol, fearing unknown risks in a new blockchain environment. Additionally, the DeFi space is becoming more crowded, MultiversX's DeFi ecosystem is maturing but has yet to fully distinguish itself from competitors which would help attract a broader base of DeFi users.

3. Insufficient On-chain Opportunities

Another factor dampening liquidity is the lack of attractive on-chain investment opportunities. Other blockchains offer more established yield farming protocols, lending pools, and liquidity incentives that attract and retain capital. MultiversX needs more compelling offerings to entice users to lock up their funds on its DeFi ecosystem, as it currently struggles to offer returns that compete with larger, more mature ecosystems. Even when attractive opportunities are available, the aforementioned issues limit their effectiveness in attracting new liquidity..

4. Barriers to Liquidity Flow

Liquidity on MultiversX is predominantly sourced through wrapped tokens via the official ad-Astra bridge. While this bridge has been audited and stress tested, it still faces considerable skepticism due to the broader history of bridge hacks in the crypto space. Non-native tokens, especially those wrapped through bridges, have often been viewed with distrust because they carry additional risks. The reluctance to use bridges is not exclusive to MultiversX, but given its reliance on wrapped tokens and lack of native stablecoins, the issue is more pronounced here.

5. Centralization Concerns

The official bridge used by MultiversX is governed by a 7/10 multi-sig, with five of the signatures controlled by the core team and the other five held by key validator partners. While this setup adds a layer of security, it also raises concerns about centralization. Many users in the DeFi space prefer fully decentralized solutions, and the fear of fund seizures or freezes due to centralized control has probably deterred some participants from bridging funds.

The vulnerabilities inherent in cross-chain bridges have emerged as one of the top security concerns within the crypto community. Although the number of bridge-related hacks has decreased in the past two years, bridges remain one of the primary targets for malicious actors due to the large volumes of assets they hold and their critical role in facilitating interoperability between chains.

Cross-chain bridges have been at the center of some of the most notorious hacks in crypto history, significantly eroding users' trust in these mechanisms. This skepticism is especially pertinent to MultiversX, where liquidity from wrapped stablecoins is a vital component of the ecosystem. Despite the foundation’s ongoing efforts to bolster the security of its bridge, the broader community remains wary, which continues to hinder the influx of new liquidity.

By addressing these core issues, MultiversX has the potential to rebuild its liquidity base and re-establish itself as a competitive player in the DeFi space. With USH aiming to solve some of these problems bringing to MultiversX a decentralized native stablecoin linked with attractive DeFi yield opportunities.

USH is an over-collateralized stablecoin pegged to the USD and represents the first native fully-decentralized stablecoin on MultiversX.

As the name suggests, an over-collateralized stablecoin is backed by a reserve of other assets to maintain its price as close as possible to the underlying asset.

Each USH is backed by different assets that are securely held by Hatom’s smart contracts. This reserve exceeds the value of USH to ensure its security and stability, in order to maintain the 1 $USH = 1$ USD ratio, that's what we call Over-collateralization Mechanism.

If the price of USH deviates from its peg at $1, an arbitrage and redemption mechanism has been developed by the protocol.

Let's imagine that 1 USH is trading for $0.95 on a DEX. In this scenario, you could buy USH at the discounted price of $0.95 and use it to repay your USH debt on Hatom at the value of $1 per token. This allows you to profit from the price difference, effectively gaining $0.05 per USH repaid.

Conversely, if USH is trading above $1 on a DEX, you could mint USH via Hatom and sell them at a higher price to make a profit.

This mechanism ensures that the price of USH remains stable and closely aligned with the USD and incentivizes arbitrageurs.

Anyone can deposit their tokens as collateral on Hatom to mint new USH in return. This USH issuance is made possible through Facilitators.

There are several facilitators that allow the issuance of USH, each offering different advantages:

Lending protocol as a Facilitator : It allows you to directly use your assets deposited in the lending protocol as collateral to mint USH. The borrowing rates are fixed and vary depending on the asset.

Isolated Pools as Facilitators : It allows the use of specific assets (EGLD & wTAO), as well as their staked versions) as collateral to mint USH without any borrowing fees.

USH also provides a source of yield for its holders through the staking module, redistributing the profits generated by the facilitators to users depositing USH LPs into this module.

USH is a unique and innovative value proposition within the MultiversX ecosystem.

First and foremost, it is the first decentralized stablecoin native to this blockchain, bringing immense potential for innovation and implementation across various protocols on MultiversX.

Being natively built on MultiversX, USH is an ESDT (Elrond Standard Digital Token). Unlike standards such as ERC20 or SPL20, which rely on smart contracts, ESDTs are not smart contracts but rather native tokens. This reduces potential vulnerabilities, lowers transaction costs, and simplifies the management of such assets.

USH is a decentralized stablecoin, meaning it is not managed by an intermediary like Tether for USDT or Circle for USDC, but rather by an autonomous protocol, in this case, Hatom.

Any user with a wallet on MultiversX can interact with USH. They can mint new USH by providing collateral as a guarantee to maintain USH's financial stability or burn some of their USH to reclaim their collateral.

As a decentralized stablecoin, USH is not subject to regulations targeting centralized entities. It also provides greater security than centralized assets, as being on-chain ensures complete transparency of the funds backing its collateral.

At any time, users can view onchain the collateral funds securing USH's price stability and trace all transactions related to this token.

USH is significantly redefining the DeFi ecosystem on MultiversX.

USH enhances liquidity across the entire ecosystem through seamless integrations with major decentralized applications on MultiversX. This will create numerous new yield opportunities for users of various protocols, while also benefiting the protocols themselves by attracting additional liquidity and driving increased trading volumes.

The unique synergy offered by Hatom across its various modules (Isolated Pools, Liquid Staking, Lending, and Booster) enables platform users to optimize the yield on their assets while also benefiting from native returns through its staking module directly integrated into Hatom. All of this while positioning HTM as the central driving force of Hatom protocol

Today, the DeFi landscape is composed of many stablecoins, whether centralized or not, algorithmic or over-collateralized, etc… Each has its own advantages and disadvantages, which must be considered before using them.

USH offers several benefits to its users :

Additionally, as a decentralized stablecoin, USH is a fully transparent stablecoin, it’s possible to track its reserves directly on-chain and ensure its overall health.

Other useful ressources :

Collateralize ratio of DAI : 157%, most important part = stablecoins

.png)

Dai metrics :

https://dune.com/steakhouse/makerdao

Stablecoins play a major role in the crypto DeFi economy, with decentralized ones being of upmost importance for a truly decentralized environment. To ensure stablecoins security, liveness and reliability, there needs to be complex mechanisms in place to ensure USH safety in all circumstances.

The main thing for a stablecoin, as the name suggests, is to keep its value pegged to the dollar. Staying safe in all conditions while providing an attractive design is the hard problem.

That is possible by being overcollaterized and implementing different peg mechanisms.

The USH minting model is based on an over-collateralization design, ensuring the value deposited as collateral always exceeds the amount of USH minted. This approach is key to maintaining the USH peg, protecting USH peg in all circumstances.For example, when a user mints $1,000 worth of USH using any of the approved collateral tokens, the protocol holds more collateral than the minted amount to back the stablecoin securely.

This over-collateralization mechanism ensures USH remains stable by consistently being backed by sufficient value, even when collateral assets prices fluctuate. Each token will have its own minting rate, allowing users to mint USH with different collateral factors.

A user mints USH by providing collateral, which is securely held in Hatom’s smart contracts. As long as the value of the collateral remains above the liquidation threshold, it will not trigger a liquidation event. However, if the collateral's value falls below this threshold, a liquidation can occur. This mechanism allows USH to maintain its peg by ensuring over-collateralized backing at all times, keeping a safe buffer to ensure liquidations can happen at any time and collateral is enough to repay the total debt.

For example, if BTC has a collateralization ratio of 70%, a user can mint up to $700 from $1000 worth of BTC. However, if the value of BTC drops, causing the borrowed amount to exceed 70% of the new collateral value, the user's collateral would be subject to liquidation.The network would be safe as long as the value minted never exceeds the value in collateral, so in this case there’s always the need for >700$ in collateral.

There are three primary mechanisms to maintain the hard peg of USH to USD:

Since USH's market price may fluctuate due to how DeFi pools operate, these mechanisms create arbitrage opportunities.

There are two possible scenarios based on the direction in which USH moves.

When USH Trades Above $1:

When USH Trades Below $1:

Liquidations also play a critical role in helping maintain USH’s price stability and peg to the USD by ensuring that every USH minted is fully backed by collateral.

Here's how it works:

Hatom introduces a novel mechanism to protect the peg in case of depegs, called redemptions. It’s similar to liquidations, but there are certain fundamental differences to better address the unique problems posed by depegging situations.

A depeg strategy smart contract continuously monitors the market price of USH and activates redemptions during a depeg.

There are some conditions to activate redemptions and avoid market manipulation:

The scope of the redemption mechanism is to activate only when the price depegs over a sustained amount of time, so that normal market dynamics have time to repeg the price naturally.

Redemptions are activated at a smart contract level in isolated pools. This essentially allows redeemers to repay USH loans with USH purchased at a discount on the market and redeem collateral from other users in isolated pools.

When USH trades below 1$, this happens:

One concrete example:

The mechanism restores the peg by increasing demand for USH and reducing the aggregate size of USH loans, with no strong penalty for users who have borrowed USH in isolated pools. Accounts are redeemed based on the health factor, calculated based on borrows and collateral ratio, improving the health factor of the riskiest accounts until the peg is restored.

Let’s get an example with Alice.

Users positions are not redeemed completely, but let’s assume it is for an easier explaination:

Her position would be valued:

When and if a redeemer repays her 100 USH loan, restoring the peg, she’d be left with:

The peg can be restored with no strong penalty for Alice (compared to a liquidation) and only losing exposure to EGLD.

The redemption mechanism, combined with the other stabilization techniques, makes USH extremely resilient and resistant to depegging events.

The three peg mechanisms guarantees that:

USH design allows USH to strongly hold its value even in hostile market conditions.

Throughout history, the power to create money has been tightly controlled by governments and central banks. This authority—enabling the issuance, management, and dilution of national currencies—has long been a pillar of the global financial system. However, with the advent of blockchain technology, tokenized assets, and smart contracts, we stand at the dawn of a financial revolution.

USH is at the forefront of this transformation. It represents a new paradigm in money creation, one that is transparent, decentralized, and trustless. Unlike fiat currencies, which derive their legitimacy from government decree, USH is backed by real, on-chain collateral and operates under immutable, publicly verifiable rules. Its facilitators are the smart contract mechanisms that govern the issuance, redemption, and economic rules of USH—acting as programmable central banks, yet without the opacity and discretionary policies of traditional financial institutions.

In the fiat system, money is created through mechanisms such as central bank lending, fractional reserve banking, and government stimulus. Yet, these processes lack transparency and are often subject to political influence. The value of fiat currencies erodes over time as money is continuously printed without direct collateral backing, leading to inflation and loss of purchasing power.

USH, however, is designed differently. Its facilitators act as transparent money-printing mechanisms, ensuring that every USH token entering circulation is backed by verifiable assets. These facilitators serve as trust anchors, enabling anyone to participate in the monetary system, provided they follow the pre-established rules.

The power of this innovation lies in its inclusivity:

This shifts money creation from a privileged, centralized process to an open, decentralized system where users become active participants in shaping a stable, digital economy.

USH is issued through four facilitators, each designed to serve distinct financial needs while maintaining peg stability and capital efficiency.

💡 Key difference from fiat: In traditional banking, loans are often issued with fractional reserves—meaning banks lend more than they hold. The lending facilitator eliminates this fragility by always ensuring full on-chain over-collateralization.

💡 Key innovation: unlike traditional financial systems, which require users to pay interest even on fully collateralized loans, this facilitator enables liquidity creation without long-term debt accumulation—a powerful financial tool for users seeking stable, cost-efficient capital.

💡 Impact: this mechanism bridges the gap between stablecoin issuance and DeFi adoption, providing stable liquidity for emerging projects without the risks of centralized market-making.

💡 Key benefit: this facilitator creates low-risk, high-liquidity stablecoin reserves, making USH an attractive option for institutional DeFi adoption. Unlike fiat reserves held in opaque banking systems, this collateral is fully auditable on-chain.

The introduction of facilitators redefines money creation in the digital age. Unlike central banks, which operate behind closed doors, the USH minting process is:

✅ Fully transparent – all transactions are recorded on-chain, auditable by anyone.

✅ Algorithmic & rules-based – supply and demand are regulated through smart contracts, eliminating discretionary decision-making.

✅ Decentralized – no single entity controls issuance, making USH resistant to manipulation.

USH’s economic model is hard-coded into its facilitators, ensuring that:

Unlike fiat currencies, which are diluted by inflation, USH’s model preserves purchasing power by maintaining a strict collateral-backed issuance framework.

The facilitators of USH represent more than a technical mechanism for stablecoin issuance. They embody a financial revolution—one that allows anyone to take part in the creation of money while ensuring absolute transparency and trust.

USH is not just a stablecoin.

It is the future of programmable money—built by the people, governed by code, and accessible to all.

Financial stability has always been rooted in the ability to secure liquidity, maintain confidence, and align incentives between market participants. In traditional finance, central banks achieve this by managing reserves, setting interest rates, and providing liquidity backstops to stabilize economies. But these mechanisms are centrally controlled, opaque, and often inaccessible to the broader public.

The USH staking module introduces a decentralized alternative—a system where liquidity providers themselves become the backbone of monetary stability, earning rewards for reinforcing USH’s liquidity and price efficiency. By leveraging permissionless smart contracts, it ensures that participation, incentives, and trust are algorithmically enforced rather than dictated by centralized authorities.

Much like how governments hold gold reserves or treasury bonds to back national currencies, the USH staking module incentivizes liquidity providers to lock value into USH’s ecosystem, ensuring deep, liquid markets while maintaining peg stability.

Liquidity is the lifeblood of any financial system. Just as commercial banks rely on deposits to fund loans, USH relies on staked liquidity to maintain depth in its trading markets and ensure price stability. The staking module accomplishes this by offering multi-layered incentives to liquidity providers, aligning their interests with the long-term health of the ecosystem.

Participants in the staking module contribute by locking liquidity provider (LP) tokens or farm tokens from decentralized exchanges (DEXs). This action serves two critical purposes:

Stakers earn rewards through up to four distinct income streams, mimicking the multi-channel income structures of traditional financial reserves:

This layered incentive structure ensures sustainable, non-inflationary rewards, much like how central banks carefully balance interest rates to optimize capital flows while preventing excessive inflation.

The USH staking module operates across multiple liquidity pools, focusing on key trading pairs that drive demand and utility within the MultiversX ecosystem. These include:

By concentrating rewards on USH-paired assets, the protocol channels liquidity into the most critical areas, ensuring that USH maintains deep, accessible markets while reinforcing its peg stability.

Unlike inflationary reward models seen in many DeFi protocols—where liquidity incentives eventually lead to unsustainable token emissions—the USH staking module is designed with long-term sustainability in mind. Rewards are not sourced from new token issuance but rather from revenue-generating facilitators, making the system more resilient and self-sustaining.

This staking mechanism represents a new generation of decentralized monetary reserves, where participants themselves become the backers of stability rather than relying on centralized monetary authorities. By doing so, the USH staking module challenges the long-standing paradigm of institutional financial control, proving that stability and liquidity incentives can be achieved through community participation and decentralized economic design.

USH staking is not merely a feature—it is an economic pillar that transforms liquidity into stability. By enabling anyone to contribute to the stablecoin’s resilience while earning sustainable returns, the staking module democratizes financial participation and reshapes how liquidity incentives are distributed in decentralized finance.

This is not just a technical innovation; it is a restructuring of financial incentives, shifting the power of monetary reserves from centralized institutions to decentralized participants. In this new model, trust is not imposed—it is earned, built, and reinforced by the very people who sustain the ecosystem.

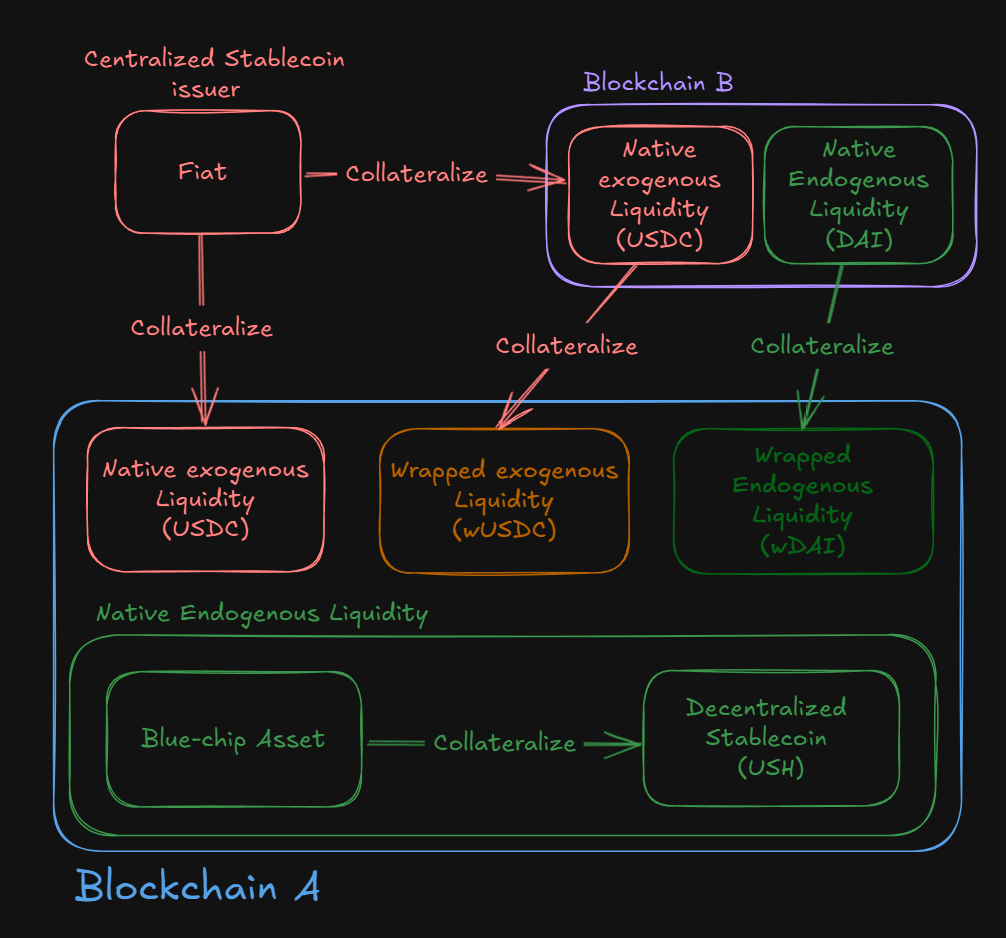

We often speak of centralized or decentralized stablecoins, but this nomenclature doesn't exactly define the nature of the liquidity from the point of view of the system that constitutes a blockchain and It's also only a high-level reduction in the diversity of stablecoins in general.

This is where we can introduce the concept of blockchain endogenous and blockchain exogenous liquidity. Depending on the nature of the asset itself, both can be native (Indigenous) or wrapped (Allogenous) to the system itself.

If we take the USDC as an example, the assets enabling collateralization are exogenous to the blockchain world, and are held either in the form of Fiat, bonds or other financial products associated with the dollar by the issuer of this stablecoin in a centralized manner. Their centralized aspect and 1:1 collateralization make them the most scalable stablecoin in terms of adoption.

These USDCs can be native, meaning that they are directly issued on the blockchain in which we hold them (blockchain A), or wrapped, meaning that they are native to another blockchain (blockchain B), and then minted on the blockchain A using a bridge that issues a new token (wrapped USDC) in 1:1 proportion to what it holds on the blockchain B.

Endogenous liquidity is, on the contrary, created directly via an asset that could not exist without blockchain. This can be the asset of the blockchain itself (EGLD, ETH) or tokens created on it (ESDTs, ERC-20s).

In the same way, Endogenous liquidity can be native to the ecosystem we're in, or wrapped from another ecosystem.

Wrapped assets can be seen as Allogenous Liquidity, since they possess trust assumptions that are independent of our own system and have no real existence here. The chain of origin as well as the bridge could be subject to a hack, a complete shutdown of operation, or other problems affecting the native asset backing the wrapped one. They too can be exogenous to the blockchain, and therefore linked to backing from the real world, or endogenous as they are backed by blockchain native assets. On the other hand, system-native assets can be seen as Indigenous Liquidity, they do not have any additional trust assumptions other than those within the system itself which enable their creation.

The four different categories created by this thinking framework make it relatively easy to understand the strengths and weaknesses of each one, in terms of the sovereignty it confers on the ecosystem, but also scalability in terms of adoption.

Endogenous Liquidity created via Collateralized Dept Positions like $DAI or $USH has a limited growth, as not being able to exceed the value of the assets used for their backing and present within their system, whereas Exogenous Liquidity is only limited by the supply of fiat money. On the other hand, the former offer maximum decentralization and sovereignty, as they are derived from the very value of the system, whereas the latter are based on a value foreign to the blockchain world, for which 1 dollar or 1 euro means nothing.

Indigenous assets compound the problems by being even less sovereign and less scalable, as they are tight to what can be migrated from another ecosystem.

This taxonomy of liquidity could even be extended on an additional dimension to this graph by adding a depth axis representing the programmatic nature of the asset, whether it is Smart-Contract based, or blockchain-standardized asset (which we often also call Native Asset, hence the importance of establishing the notion of Indigenous Liquidity so as not to confuse the two definitions). This would enable us to grasp their safety characteristics in relation to their use, holding and programmatic dependencies.

Any ecosystem that wants to grow needs to maximize the scalability and sovereignty of its liquidity, which is why having both Native Fiat-Backed and CDP stablecoin are so important.

The USH stablecoin will meet one of his needs, and the xMoney stablecoin with USDX, EUROX and RONX the other.

For the time being, wUSDC is the most widely adopted stablecoin in our ecosystem, and the complexity of the following graph representing all the dependencies and trust assumptions necessary for its use, serves alone to understand the importance of having true Endogenous and Indigenous liquidity in MultiversX.

Here we can see the current liquidity topology on MvX for the most liquid assets, on xExchange, Hatom, and the various listings on CEX.

The first thing to note is that all assets are backed by EGLD. This can be very good for EGLD when you have highly integrated ecosystem tokens on exchanges with independent productivity and growth, as their buying pressure feeds back into EGLD. On the other hand, it can also become a burden when these tokens undergo a loss of value which is directed towards an outflow in USDC, of which the EGLD<>USDC pool is the only way out.

Secondly, as the ecosystem's token pairs are denominated in USDT on all exchanges, a potential drop in the price of EGLD would drain the liquidity of these tokens on the exchange via three-point arbitrage as arbitrage can only be done via EGLD<>Stablecoin pools, making this liquidity difficult and expensive to maintain when the market is bearish.

Then, this topology leaves Ashswap's USDC<>USDT pool relatively unused, its only benefit being to enable arbitration with the relatively small EGLD<>USDT pool, and USDC<>USDT exchanges when borrow APR on Hatom can be arbitrated.

Finally, having an EGLD-only LPs encourages projects to compete for the same share of available EGLD. While this may push the ecosystem to be more competitive, it remains a long-term limitation in terms of growth, when they could instead seek to maximize their stablecoin liquidity, which grows with the industry as a whole.

Now, here's the topology that will be available at the launch of USH. All USH and EGLD LPs will now be connected in a symbiotic system, and rather than having as at present an EGLD<>USDC pair that acts as an exit liquidity for all exchanges going from ESDT to USDC, the EGLD<>USH LP will now be at the center of the system, the most interconnected in the ecosystem, and probably generating the most volume.

This not only multiplies the routes available in the ecosystem, but also drastically increases the opportunities for arbitration towards a system that will naturally seek towards efficiency. This will not only enable aggregators and DEXs to generate more volume and revenue, but also allow new strategies to be implemented within the ecosystem. As MEV is relatively difficult to achieve on MvX due to transaction random ordering, this could give way to existing community arbitrage vaults using Hatom as a fall-back mechanism to generate Yield, and use liquidity where necessary for this kind of strategy.

The more initiatives of this kind compete, the more they will return an important part of the revenues generated to the chain via fees, and enable the chain to move a little closer to sustainability.

In another dimension, this will also enable the blockchain to be truly sovereign over its liquidity, as we will no longer rely solely on Off/On-Chain arbitrage to peg EGLD to its price on Centralized Exchanges where liquidity is most important. As the price of EGLD rises, the collateralization and minting potential of USH will also increase, enabling EGLD<>Stablecoin pools to be arbitraged directly within the ecosystem by correlating its own leverage, rather than waiting for liquidity to move from Binance to xExchange, for example.

This will enable a price closer to that of the CEX at all points in time, giving a fairer price to on-chain users, but also fueling the necessary incentives to grow our own liquidity, improving the efficiency of the Lendings Protocol and their liquidation.

Compounding all these benefits with highly valuable liquidities, such as BTC, ETH, TAO, SOL, will not only allow, by aligning incentives, to see players already present in the chain specialize in more complex market making strategies, but also incentivize the development of more complex AMMs such as CLMM (Concentrated Liquidity Market Maker) and CLOB (Central limit OrderBook). The more we expand on-chain liquidity, the easier it will be to attract specialized and institutional players to play with it thanks to the growing DeFi stack on MultiversX.

Stablecoins have fundamentally reshaped financial markets, powering the rise of DeFi and altering how value is exchanged globally. Today, the daily on-chain stablecoin transaction volume exceeds $50 billion, with peak volumes surpassing $1 trillion between 2021 and 2022—a figure comparable to nearly one-fifth of global FOREX market activity.

USH enters this landscape as MultiversX’s first native, decentralized stablecoin, positioning itself to capture a share of this ever-expanding market.

For retail users, stablecoins serve as:

For institutions, the adoption of stablecoins presents:

USH, fully over-collateralized and transparent, emerges as a trustless alternative in a market where centralized stablecoins dominate. The liquidity bootstrap phase alone saw over 600,000 EGLD deposited, valued at over $30 million at the time, underscoring strong early demand for this new financial primitive.

The emergence of stablecoins like USH signals a shift in how money is created, stored, and transacted. Unlike traditional currencies, which are governed by central banks with opaque monetary policies, USH operates within an immutable and transparent framework, where rules are encoded on-chain.

Traditional financial system:

Decentralized stablecoins like USH:

As decentralized finance continues to mature, USH represents an alternative financial rail, one where users are no longer dependent on traditional banking infrastructure to transact, save, and invest.

Despite the global digitization of financial services, nearly 30% of the world’s population remains unbanked due to factors such as high costs, restrictive regulations, and lack of banking access. Stablecoins provide a bridge by offering:

USH takes this accessibility a step further through its integration with xPortal Wallet, allowing users to:

This use case effectively turns DeFi collateral into functional, spendable capital, expanding the role of decentralized stablecoins beyond crypto-native transactions into everyday financial interactions.

USH’s properties make it a powerful tool for a broad spectrum of use cases:

As the first decentralized stablecoin native to MultiversX, USH sets a precedent for how stable liquidity can fuel an interoperable, self-sustaining digital economy. By combining stability, accessibility, and programmability, it is not just a financial instrument but an enabler of new economic possibilities—both on-chain and in the real world.

Innovation is rarely recognized as a revolution in the moment. Most of the time, it appears gradual—a natural improvement over what came before. Yet, in hindsight, these shifts are seismic. The printing press did not seem like an upheaval; it was just a better way to copy books. Electricity was, at first, just an alternative to gas lamps. The internet itself was dismissed as a niche tool for academics. Today, blockchain technology faces the same skepticism. It is not loud, not visible like artificial intelligence—but beneath the surface, it is reshaping the very foundation of how economies function, trust is established, and value moves across the world.

Stablecoins have become the lifeblood of this new economy, seamlessly transferring trillions of dollars across global markets with efficiency unmatched by any traditional system. Yet, until now, true digital-native money—one that is decentralized, over-collateralized, and fully transparent—remained elusive.

USH is not just a stablecoin. It is a financial instrument designed for the internet itself—a currency that is trustless, open, and entirely verifiable on-chain. Backed not by opaque reserves but by digital assets native to blockchain ecosystems, USH represents a financial model where money is governed by protocol, not policy.

For centuries, money was backed by resources of its time—gold, silver, and oil. These were not just symbols of value but productive assets that powered economies. Today, the world is digital, and value flows not through paper notes but through blockchains, secured by assets like Bitcoin, Ethereum, and EGLD.

This is where USH emerges as the currency of a new era. It is not just pegged to the dollar—it is rooted in the decentralized economy. It is the medium of exchange for an on-chain financial system that no central entity can freeze, dilute, or manipulate.

Its launch marks a turning point for MultiversX. DeFi will no longer rely on external stablecoins; liquidity will be native, deep, and transparent. Users can leverage their digital assets not just for DeFi but to bridge finance with everyday life—spending USH directly, seamlessly merging digital liquidity with real-world economies.

"Money moves like water." Said economist Bill Phillips, It always finds the path of least resistance, flowing toward the most efficient, transparent, and accessible financial system available. Throughout history, every attempt to confine money—to resist its natural movement—has ultimately failed. From capital controls to currency pegs, from financial gatekeeping to artificially constrained markets, value has always found its way forward. The rise of USH and decentralized stablecoins is not a choice, but an inevitability. Those who embrace this shift will shape the future. Those who resist it will watch as the currents pass them by.

USH is more than a stablecoin. It is an invitation—to participate in a world where money is truly free, borderless, and built on trustless, unstoppable foundations. The question is no longer if decentralized money will reshape the economy, but how soon.

Articles published on Astrarizon Reflection Portal do not constitute legal, financial, or investment advice. Any action taken upon the information shared on Astrarizon.com is strictly at your own risk. Users are advised to conduct their own due diligence and consult with appropriate professional advisors before making any decisions.